Your Pitch Deck Says Platform. Your P&L Says Sweatshop. The Market Already Knows Which One You Are.

You price like a product company. You deliver like a services company, and compete effectively in neither. You lose deals to both. This is that story.

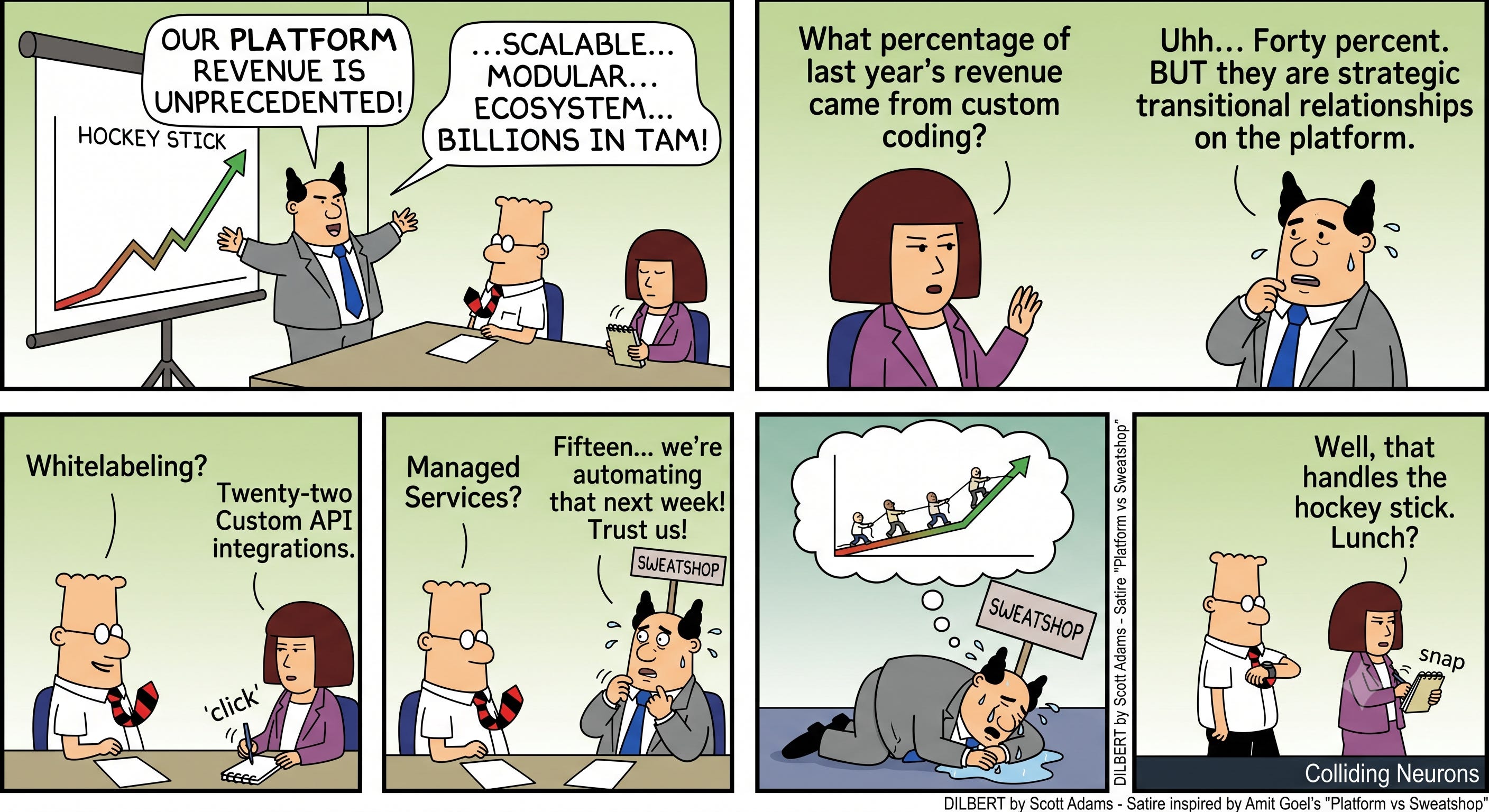

The deck has 47 slides.

Twelve of them say “Platform” in some form. Three have diagrams with concentric circles proving, architecturally, that yes, this is a Platform. Slide 22 has a Gartner quote that cost $15,000 and says absolutely nothing. Slide 38 has the hockey stick — the one that goes flat for two years and then shoots vertical, which in this context means “please stop asking questions and trust the process.”

The founder has been presenting for twenty-two minutes. He has used the words “scalable,” “modular,” and “ecosystem” with the confidence of a man who genuinely believes that saying them often enough makes them true.

The CFO has been sitting at the end of the table for twenty-two minutes without saying a word. She is the only person in the room who has read the actual financials from last year. Not the investor summary. Not the board pack narrative. The actual line items, in a spreadsheet, sorted by revenue source. This is her job. She has done it with the patient precision of someone who already knows the answer and is waiting for the right moment.

She raises her hand.

CFO: “What percentage of last year’s revenue came from custom development?”

The founder’s presentation energy adjusts. Not much. Just slightly. Like a man whose GPS has suggested a different route.

Founder: “About forty percent. But those were transition clients. They are moving to the platform.”

CFO: “And whitelabeling?”

Founder: “Twenty-two percent. But those are strategic relationships.”

CFO: “And managed services?”

Founder: “Roughly fifteen percent. We are building automation to replace most of that.”

She nods. The nod of someone who has done the arithmetic before walking into the room.

CFO: “So seventy-seven percent of your revenue last year came from billing people’s time and building things specific to individual clients. The remaining twenty-three percent — the actual platform revenue — grew how much year on year?”

Pause. A significant one.

Founder: “Eight percent.”

CFO: “While your engineering headcount grew?”

A longer pause.

Founder: “Thirty-one percent.”

She closes her notebook. She does not say anything. She just closes it. This is somehow more devastating than whatever she might have said.

CFO: “Which part of that is the platform business?”

Nobody answers. The founder advances to the next slide.

It says Platform.

I have been in some version of this meeting more times than I would like over last few years. The industry changes. The deck gets updated. The hockey stick gets redrawn with slightly more optimistic assumptions each iteration. The CFO’s question, however, is constant. And the founder’s answer — transitional, strategic, nearly finished, next year will be different — is always the same answer wearing different clothes.

Next year is the most popular destination for product companies that have never actually left the services business. Almost nobody arrives.

This article is about why. And about the handful of companies that figured out what they actually were, used that clarity as a competitive weapon, and left everyone else holding a deck with a hockey stick on slide 38.

The Question That Changes Everything

Michael Porter published Competitive Advantage in 1985. Forty years later, the single most consequential idea in that book is still being actively ignored by most B2B software companies, often by the same people who cite Porter in investor calls.

Porter’s Five Forces framework is taught in every MBA program as a competitor analysis tool. That is not what it is. It is a framework for understanding the structural economics of an industry and identifying where a defensible competitive position actually exists. And his deepest, most consistently avoided insight was this: being stuck in the middle is the most dangerous position in any market.

Porter’s Generic Strategies. The middle is the danger zone. Too expensive to win on price, too undifferentiated to command a premium. Most B2B software companies move here voluntarily and call it “flexibility.”

Choose cost leadership, or choose differentiation. Build the lowest-cost operation in your category, or build something genuinely distinct that commands a premium. The company stuck in the middle is neither cheap enough to beat the low-cost players nor different enough to justify the premium. It gets beaten from both directions simultaneously and genuinely cannot understand why, because the strategy document looked perfectly sensible when it was written.

Now read that again and think about every B2B software company that prices like a product company in the sales pitch, delivers like a services company in execution, recruits like a product company in the job description, and measures success like a services company at the end of every quarter.

That is not a growth strategy. That is a Porter case study being authored in real time, by people who studied Porter and are now living inside his example.

The honest first question — before roadmaps, before pricing models, before any conversation about competitors — is the one the CFO asked. What does money actually flow to you in exchange for?

If the answer is access to technology that works identically for every customer, you are a product company. If the answer is people’s time, expertise, customized delivery, and managed outcomes using technology as the vehicle, you are a services company. Both are legitimate. Both have produced enormous businesses. The destruction begins when you refuse to answer honestly and default to whichever identity currently has the better valuation multiple.

The Economics Are Not Negotiable

In 1998, Hal Varian and Carl Shapiro published Information Rules, a book about the economics of information goods. Varian later became Google’s Chief Economist. The central argument is precise and still systematically under-internalized: software, data, and any product you can copy without destroying the original operates under fundamentally different economics from physical goods and human services. The first copy costs you everything. Every copy after that costs you almost nothing. This is the zero marginal cost principle.

A services business runs on one equation: revenue equals people, multiplied by rate, multiplied by utilization. Every variable is human. To double revenue, you roughly double the people delivering the service. The ceiling is always headcount. Accenture has approximately 738,000 employees and generates around $65 billion annually. Those numbers move together. This is the correct mathematical behavior of a well-run services business.

A product business runs on a different equation: revenue equals users multiplied by monetization rate, where the marginal cost of adding the next user approaches zero as infrastructure scales. The software is the same product for customer 500,000 as for customer 5. You do not rebuild it. You add a row to a database and collect the revenue.

The hockey stick is a precise mathematical description, not a slide decoration. It only appears when marginal revenue substantially exceeds marginal cost. In a services business, they move together. Always.

This is why investors pay 10 to 20 times revenue for SaaS companies and 1 to 2 times for services businesses. It is not irrational. It is a rational price for two different growth trajectories — one that compounds and one that does not.

Daniel Kahneman described what he called the narrative fallacy — the human tendency to construct stories about why things are happening that feel coherent and inevitable but are post-hoc rationalizations. Founders are among the most gifted narrative fallacy practitioners on earth. The story goes: we are taking services revenue now to fund the platform, and once the platform matures, the services will fall away. This story is told in every B2B startup boardroom on every continent. It is almost never true. Not because platforms fail to get built. Because of what happens to the organization in the years spent building them.

Culture Does Not Read the Strategy Document

The phrase most widely attributed to Peter Drucker — “culture eats strategy for breakfast” — has been turned into a motivational poster, a conference keynote opener, and the kind of thing people say at offsites between the team lunch and the afternoon workshop on Q3 priorities. None of this has diminished how precisely and devastatingly true it is.

Six words. Forty years of organizational evidence. The strategy document is aspirational. The daily incentive structure is operational. Only one of them runs the company.

What it actually means is this: the daily operating reality of an organization — what gets rewarded, what gets deprioritized, what happens when two priorities conflict at 4pm on a Friday — will always defeat a document. Strategy is a declaration of intent. Culture is ten thousand daily decisions made by real people with real incentives and real performance reviews. Ten thousand daily decisions beat a declaration before the ink dries.

A company that earns most of its revenue from custom development, managed services, and whitelabeled deployments builds a very specific organizational culture without intending to. It hires delivery managers who are excellent at client management and scope negotiation. It hires account managers who are measured on expansion revenue — which means they are structurally incentivized to promise whatever is required to close the deal, because the consequences of that promise land on the product team three weeks later as a Slack message titled “quick question / client request / just a small thing.”

Now a senior product manager joins. Her LinkedIn announcement says she is “excited to be joining this rocketship to build a category-defining platform.” Her offer letter mentions vision, roadmap ownership, and product-market fit.

Her first sprint is forty percent dedicated to a custom date-picker component for a client paying $11,000 a year, because the account manager confirmed in the sales call that this would “absolutely not be a problem.”

Her second sprint is rebuilding the export function to include three columns that one client needs and no other client has ever asked for. The client has been on the platform for eight months and has generated $14,000 in total revenue.

Her third sprint is a whitelabeling configuration for a client paying $8,000 per year for what cost, in real engineering time, approximately $35,000 to set up and will cost another $15,000 per year to maintain. Nobody has done this math. The person who would do the math left six months ago to join an actual product company.

By month five, she has a Notion document titled “Product Roadmap Q2.” It has forty-seven items and zero prioritization. It has not driven a single sprint. The sprint is driven by what the account team closed last quarter and what three clients emailed this week. The roadmap document is a piece of fiction that exists to be shown at board meetings.

By month eight, she is either updating her resume or she has made her peace with being a business analyst embedded in a client services operation that calls itself a product company.

IBM is the canonical long-form version. Global Services grew through the 1990s into the world’s largest technology consulting operation. By the mid-2000s, it was the organizational center of gravity. IBM sold its PC division to Lenovo in 2005. Its server division went in 2014. The organizational will to protect product businesses from services revenue — one client escalation at a time — had simply run out.

Every major Indian IT firm has a product division. Infosys built Finacle. Wipro built Holmes. HCL built DryIce. None became product companies. Because you cannot override the incentive structure of 200,000 people organized around billable client delivery with a product launch and a press release.

Who Is Your Real Competitor? (This Is the Part That Hurts)

The company’s competitive matrix shows favorable positioning against Salesforce, HubSpot, and two well-funded SaaS businesses with genuine product-market fit. The matrix has green checkmarks arranged to suggest superiority. It has been in every board deck for three years.

Last quarter, the company lost four deals.

The first went to a development agency in another city that quoted a custom build at $38,000. The agency does not have a platform. It has eleven engineers, a Basecamp workspace, and a willingness to build exactly what the client asked for at the price the client wanted to pay. The agency won.

The second went to a regional system integrator that has been in the client’s office every quarter for four years. The integrator knows the client’s CFO by name. The integrator does not have a roadmap. It has relationships. The integrator won.

The third (this one stings) the prospect decided to build it internally after a recently hired developer said “we could build this in about six weeks.” The developer was optimistic by approximately eighteen months, but nobody found that out until later.

The fourth they lost to the cheaper whitelabeling competitor. The competitor’s product is objectively worse. It is also $40,000 a year less expensive. The competitor won.

None of these four competitors appear in the competitive matrix. Not one. The matrix features Salesforce, which has never once competed for the same deal.

This is the identity crisis in its most expensive form. A company earning seventy-seven percent of its revenue from services is competing in the services market whether or not the pitch deck says otherwise. And in the services market, the competition is not the product company on the TAM slide. The competition is the development agency billing $45 an hour. It is the system integrator with better relationships. It is the client’s own IT team on a motivated Tuesday.

The tragedy is architectural. The product company you are trying to be will beat you on marginal economics and distribution — because those are the advantages of a product model you have not built. The services company you actually are will beat you on price, flexibility, and relationship depth — because those are the advantages of a services model you are pricing yourself out of by insisting you are not one.

You lose to the product company because your model cannot match its economics. You lose to the sweatshop because your pricing assumes you are not one. Porter called this getting beaten from both directions simultaneously. He described it in 1980.

The Commoditization That Was Never the Problem

Nobody talks about AltaVista. Nobody puts Friendster on their list of formative products. Blackberry built genuinely superior mobile email years before Apple entered the phone business. It had over 80 million subscribers at its peak. It was used by presidents and heads of state and every investment banker who needed to feel consequential at 6am. The engineering was excellent. Blackberry is now a cybersecurity licensing company.

The received wisdom in competitive markets is that the best product wins. It is an appealing story, particularly for engineers. It is wrong with sufficient regularity that building a strategy around it is genuinely dangerous.

WebEx was founded in 1995. Cisco acquired it in 2007 for $3.2 billion. By 2011, video conferencing was mature, well-funded, and thoroughly commoditized. Eric Yuan was VP of Engineering at Cisco WebEx. He understood the codebase, the user frustration, and the competitive landscape better than almost anyone alive. He left Cisco in 2011 to start Zoom. His investors were politely skeptical. Video calling was a feature dressed up as a company.

Zoom did not build better video. It made one product decision differently: you could join a meeting without creating an account. One link. No plugin installation. No sign-up friction for the person on the other end. That single decision about where to put the friction restructured the entire distribution model. By 2020, Zoom had 300 million daily meeting participants. WebEx had been in market for 25 years. Nobody told their grandmother to install WebEx when offices closed in March 2020. Zoom had won the verb.

Clayton Christensen spent decades at Harvard studying why incumbents lose and arrived at an insight his consulting clients kept trying to argue with: customers do not buy products. They hire products to do a specific job. Zoom was hired to do one job — let someone join a call without preparing for it. WebEx could technically do that job. It refused, through accumulated friction and enterprise-first design philosophy, to actually deliver it.

The same pattern: Slack launched in 2013 as a pivot from a failed video game, against HipChat, owned by Atlassian — a $10 billion company with a natural cross-sell base. Atlassian shut HipChat down in 2019 and migrated its own customers to Slack. Figma entered a market where Adobe had been the professional design standard for 25 years. Adobe tried to acquire Figma for $20 billion in 2022. Regulators blocked it. Figma is independently valued at approximately $12.5 billion.

In adtech: The Trade Desk. In 2009, every DSP was chasing the same story — disintermediate the agency. Jeff Green made the exact opposite call. The Trade Desk would serve agencies exclusively. It would never go direct. It would never compete with the buyers on its own platform. When the entire industry was building roads that bypassed agencies, TTD was building the best possible road for agencies to use.

This was not a technology decision. DataXu existed. MediaMath existed. The real-time bidding infrastructure was not proprietary. What TTD built was a positioning decision made in explicit contradiction to the market consensus. TTD did whitelabel — once, for Walmart, at a price that covered the full engineering overhead and maintenance cost for multiple years. The deal funded the platform rather than fragmenting it.

The correct price for whitelabeling is the price at which the economics are honest. For most B2B SaaS businesses, that number starts at somewhere between uncomfortable and “the client just ended the call.”

A Hundred Companies That Could Have Won

For every Salesforce, there are roughly a hundred CRM implementation firms with better domain knowledge, deeper client relationships, and engineers who had built CRM systems for specific industries before Marc Benioff incorporated in 1999. Several had technically superior solutions. None of them built a company worth anything close to what Salesforce became.

What they could not do was say no to the client on the phone in order to build for the market they could not yet see.

This is the actual moat of a product company. Not the IP. The repeated, compounding, organizationally painful decision to build for a market at scale rather than customize for the client at hand. Every time a company with product ambitions takes a custom contract below its real cost, builds a bespoke feature for one client because the account manager needs to close the quarter, or whitelabels at a price that requires subsidizing the client’s vanity from the core product budget, it makes a micro-decision that moves it one increment toward the linear growth curve. No single decision destroys the product company. A thousand of them do.

Theodore Levitt argued in Marketing Myopia in 1960 that companies fail when they define their business too narrowly. The reverse failure is equally fatal: companies that define their aspiration too broadly while daily operations remain too narrow. Companies with a TAM slide for a market they are not competing in. Companies whose competitive matrix lists Salesforce and whose lost deals go to a development agency charging $40 an hour.

Back in the Conference Room

It is now eleven forty-five. The slides are done. The founder has answered every question with some variation of “strategic,” “transitional,” and “we are building the automation for that.” The CFO has written two things in her notebook and shared neither.

The honest version of this conversation — the one nobody delivers because the incentives do not reward it — goes like this.

If most of your revenue comes from selling people’s time, own it. Build a delivery operation that is genuinely excellent. Price the services at what they are actually worth. Stop hiring engineers with the platform narrative and then assigning them to client customizations. Stop putting Salesforce in your competitive matrix when your actual lost deals go to cheaper implementation shops. Stop raising capital at software multiples for a business whose growth model is linear, proportional, and headcount-dependent.

If you genuinely intend to build a product company, make the decisions product companies make. Protect the marginal cost economics at the moment when services revenue is easier. Price whitelabeling at what it actually costs. Build distribution that works without adding a person. Accept that the hockey stick requires years of apparently flat growth before the inflection — and do not dismantle the model in year two because the quarterly number is uncomfortable.

There is nothing wrong with being a services company. Deloitte does not have a SaaS product and is worth more than most software companies. McKinsey does not have a platform and has never needed one. Accenture generates $65 billion on a pure services model. These are excellent businesses, run with genuine craft and priced correctly for what they deliver.

The Trade Desk made one decision in 2009 and held it for fifteen years. Against well-funded competitors. In a commoditized market. With technology that was not uniquely proprietary. The consistency — not the features, not the infrastructure — is the moat. Fifteen years of every organizational decision reinforcing the same honest answer to the question the CFO asked.

Your pitch deck says Platform.

Your P&L says Sweatshop.

Your CFO knows which one is true.

And if you are still not sure, go back to slide one and count how many times it says “platform.”

Then look at who you actually lost your last deal to.

That will sort it.