SaaS Is Not Dead. But Your Subscription Pricing Model Is.

Software is growing. Service is growing. Usage is growing exponentially. What is ending is the 20 year arrangement where the customer who barely logs in pays the monthly invoice without any outcome.

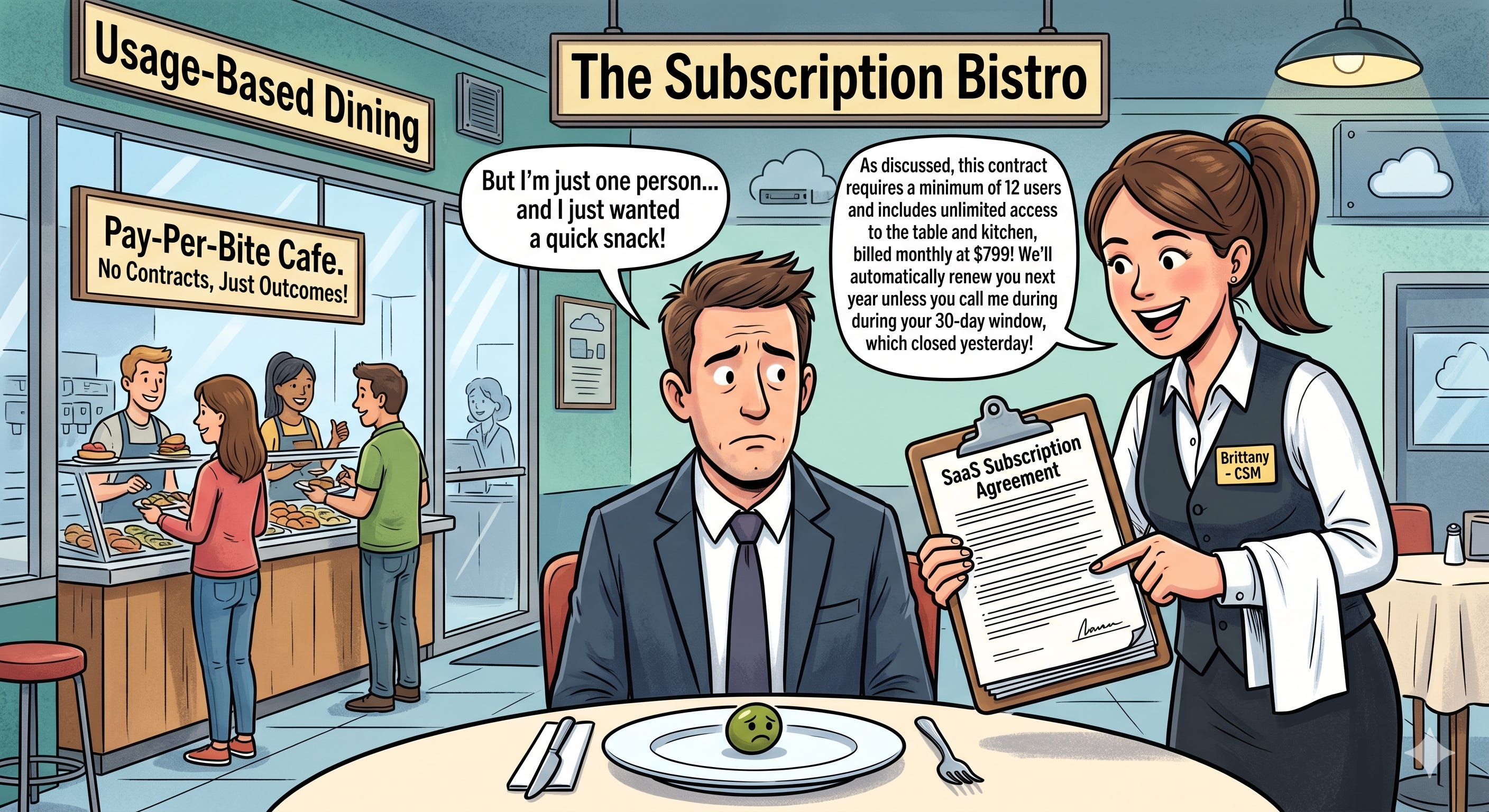

I. The Restaurant That Charges You Before You Sit Down

There is a restaurant in your city. It has decent food, a competent kitchen, and staff who respond to emails in two to three business days. You want to try it. You walk in. The maitre d’ greets you warmly, hands you a menu, and then, before you have looked at a single dish, slides a contract across the table.

The contract explains that your monthly fee is $799 and covers access to the dining room, the kitchen, and the wifi password. You will be billed on the first of every month, regardless of how many times you visit. If you come every day, great. If you come once and spend the next eleven months eating at home because the risotto was too salty, that is technically your problem. You are also required to pay for twelve users. You have explained three times that you only eat alone. They have explained that their pricing is per seat, and a table of twelve is a table of twelve.

You politely ask what happens if the food is bad. The contract has an answer for this too. There is a 30-day cancellation window, which opened the day you signed, closed 27 days ago, and will reopen 335 days from now. There is a customer success manager assigned to your account. Her name is Brittany. She will schedule a call.

Across the street, there is another restaurant. No contract. No seat minimum. You pay for what you eat. The food is good, and when it is not, you did not pay for it. The owner does very well on the nights when the restaurant is full and very little on the nights when it is not. But the owner has also noticed that the more people enjoy the food, the more food they order. Revenue and quality point in the same direction. Nobody needs to call Brittany.

This is, in its essential structure, the story of what is happening to enterprise software in 2026. Not because anyone invented this idea recently, and not because artificial intelligence discovered economics. Because two things happened simultaneously that made the old contract impossible to defend: the cost of building software fell off a cliff, and customers got much, much better at doing the math.

* * *

II. What Is Actually Dying: The Seat, Not the Software

Before going further, a clarification is needed, because the “SaaS is dead” discourse has produced a small cottage industry of wrong conclusions. Software as a service is not dying. The delivery model, software running in the cloud, updated continuously, accessible from a browser, maintained by the vendor, is thriving. The SaaS market was approximately $317 billion in 2024 and is growing at roughly 20 percent annually according to BetterCloud’s 2025 survey of IT decision-makers. That is not a dying market.

What is changing is the payment model. For two decades, SaaS companies have priced their products the same way a landlord prices an apartment: a fixed monthly amount, per occupant, regardless of whether the occupant cooks dinner every night or travels for three months and leaves the lights on. The metric was seats. The formula was seats multiplied by price equals MRR. Monthly Recurring Revenue multiplied by twelve equals ARR. ARR was the number that VCs used to value companies, that founders used to raise money, and that sales teams used to forecast. ARR was the religion. The seat was the deity.

The problem with the ARR religion is that it creates a perfect misalignment between what the software company cares about and what the customer actually needs. The software company cares about seat count and churn rate. The customer cares about whether the software is making their business better. These goals can be compatible. They often are not. A customer who buys 50 seats and uses 12 is still paying full price. A customer whose business doubles in size and needs the software twice as much pays exactly the same as before unless they add seats, which requires a sales conversation, which requires a renewal cycle, which requires Brittany.

Usage-based pricing solves this misalignment at the root. The metric changes from seats to usage. How many actions did the software perform? How many tokens did it consume? How many API calls were made, how many automations ran, how many tickets were resolved? The customer pays for what the software does, not for the right to access it. Revenue grows when the software grows in value to the customer, automatically, without a sales cycle. This is the shift. Not the death of software. The death of the seat.

* * *

III. When the Seat Dies, the Spreadsheet Dies With It

Here is where it gets uncomfortable for every CFO who built a three-year model on ARR projections: when the pricing unit changes from seats to usage, the predictability that made ARR so beloved evaporates. MRR and ARR assume a fixed revenue per customer per period. Usage-based revenue has no such assumption. It varies with customer behavior, with seasonality, with how aggressively the customer deploys the software, with whether they had a good quarter.

A company that switched one of its customers from a $10,000 per month seat license to a usage-based model might see that customer generate $4,000 one month and $18,000 the next. Averaged, it is more revenue. But averaged revenue requires a different mental model from the investor relations call, from the board deck, and from the sales compensation plan. The traditional dashboard showing MRR, ARR, net revenue retention, and logo churn starts to look like a description of a business you are no longer running.

VCs are already rewriting their frameworks. According to a 2025 analysis from Drivetrain, investors now ask AI-native companies to present ARR plus annualized usage as a combined metric, sometimes called a hybrid run rate, to capture both the stable subscription base and the variable consumption layer. The metric is messier. The story it tells is more accurate. Some investors have started tracking “inference whales,” customers who generate 175 times more in usage than they pay in subscription fees, which is a wonderful problem to have except when your pricing model was not designed to capture it.

The focus shifts from growing the user base to growing usage per user. DAUs and MAUs, the consumer metrics imported into enterprise SaaS to prove engagement, matter less than actions per user per session, tokens consumed per customer per quarter, automations triggered per account per month. The question stops being “how many people have a login” and becomes “how much is each person actually doing.” For the first time, the software company’s financial incentives are aligned with the customer getting real value out of the product every day. This is not a minor adjustment. It is a different business.

* * *

IV. Nadella Pulled the Fire Alarm. Here Is What He Actually Said.

In December 2024, Microsoft’s Satya Nadella went on the BG2 podcast with investors Brad Gerstner and Bill Gurley and said something that landed differently depending on what you were listening for. Most people heard “SaaS is dead.” What he actually said was more specific: the architecture of enterprise software is going to collapse into an AI layer that sits above the databases and manages the business logic that used to live inside individual applications.

“The notion that business applications exist, that’s probably where they’ll all collapse in the agent era, because if you think about it, they are essentially CRUD databases with a bunch of business logic. The business logic is all going to these agents, and these agents are going to be multi-repo CRUD. So they’re not going to discriminate between what the back end is.” — Satya Nadella, BG2 Podcast, December 2024

The architectural point is real and important. But it is downstream of the pricing point. The reason the architecture changes is not primarily because AI is clever. It is because when business logic moves to an AI layer that operates continuously, processing data without human input, the usage profile of that software becomes fundamentally different from a human clicking through menus. The AI agent does not log in for four hours and log out. It runs. The usage-based model is not just philosophically better for this kind of product. It is the only model that captures the revenue that the product is actually generating.

The 8VC investment team, in their March 2026 essay on software value, framed what actually survives the architectural shift clearly: “Software isn’t stored code, it’s embedded judgment. An opinion about how specific people do specific work, encoded in a durable system. Taste, brand, customer success, trust -- none of that gets easier to replicate because the next foundation model ships.” The companies whose embedded judgment is scarce will survive regardless of pricing model. The companies whose value is primarily the code, and who have relied on the seat license to extract rent from it, are the ones who should be paying attention.

* * *

V. The Arithmetic That Subscription Boards Do Not Want on Slide Five

The scale argument is worth doing once, because it illustrates why the usage model is not just better but exponentially better for any software company that actually believes in its product.

There are approximately 8.2 billion people on earth. The cohort aged 18 to 60 is roughly 4.8 billion. Of those, UNESCO and OECD data put the computer-literate, internet-connected population at around 50 to 54 percent. That gives you approximately 2.4 billion people who could in theory pay for a software subscription. If every single one of them paid $20 per month for one product, the total annual revenue across the entire addressable market would be $576 billion. The absolute ceiling. The number you could reach only if you had zero churn, zero competition, and every government on earth mandated your software as compulsory.

The realistic ceiling, adjusting for purchasing power in markets where $20 a month is not a minor discretionary purchase, brings the actual paying universe down to somewhere between 600 and 800 million people globally. At $20 per month, that is $144 to $192 billion annually, maximum, for one product and that’s the TAM, the whole market size. A large number, finite, linear and that ends. Without any exponential growth factor.

Now consider the usage side. Anthropic’s API for Claude Sonnet is priced at approximately $3 per million input tokens. One enterprise customer running AI-powered document processing, customer service agents, and data analysis pipelines might consume 10 to 50 billion tokens per month. That is $30,000 to $150,000 from one customer, one month, in compute alone. Multiply that across thousands of enterprise customers, add the agentic workflows running continuously without human input, and the revenue scales with the customer’s actual use of the product, not with the number of humans who have a login. There is no ceiling visible from here. This is why OpenAI’s API revenue has been growing several times faster than its subscription revenue. The $20 subscription is the cover charge. The API is the bar.

* * *

VI. Adtech Already Ran This Experiment. Twenty Years Ago. For Free.

While enterprise SaaS spent two decades refining its annual contract templates, the advertising technology industry ran the same experiment and reached the same conclusion. Nobody charges for the software. The margin is the business.

Magnite, the largest independent sell-side platform for publishers, generated over $620 million in revenue ex-TAC in 2024. It serves over 1,500 premium publishers globally and holds approximately 30 percent of the connected television programmatic market. Publishers pay nothing for the platform. Magnite takes a percentage of the advertising revenue that flows through it. According to its filings and investor analysis, take rates ran at approximately 14.5 percent historically, with the revenue mix shifting toward higher-margin CTV and curated private marketplace deals that command better economics. The software is the cost of doing business. The transaction fee is the revenue.

Index Exchange, the other major independent supply-side platform, has taken this alignment further with what it calls Transparent Dynamic Take Rates, introduced in October 2025. Rather than charging a fixed percentage on every impression, Index adjusts its fee per impression in real time based on auction conditions. If taking a smaller margin wins an impression that would otherwise have gone unsold, Index takes less and keeps the publisher whole. The Guardian tested this against a control group and reported incremental revenue without any changes to floor strategy. Index’s documentation states it plainly: publishers always receive a payment reflecting an amount equal to or greater than their contractual revenue share, and every adjustment is fully auditable through impression-level logs. The platform and the publisher now have identical incentives. Index only makes more money when the publisher makes more money.

This is not a new idea. It is the correct idea, and it is twenty years old. The reason it took enterprise SaaS this long to arrive here is that enterprise buyers were willing to pay the flat fee for long enough that the model seemed to work. The model was always subsidized by inertia and switching cost. As those two props weaken, the model requires a genuine justification. The genuine justification for a flat fee requires that the value the customer receives is reasonably stable and predictable. When AI makes software far more powerful for heavy users than light users, and when agent-driven usage patterns make some customers generate a hundred times more value per month than others, a flat fee is no longer an approximation of value. It is a fiction.

* * *

VII. The Graveyard of Vendors Who Charged Publishers a Monthly Fee

The clearest proof that subscription pricing fails when applied to customers under financial pressure is what happened to every ad tech vendor that tried to charge publishers a monthly software fee.

Publishers have been in a slow-motion financial emergency since approximately 2015. Digital advertising CPMs declined as programmatic made inventory abundant. Google and Meta absorbed the majority of advertising budget growth. Third-party cookies began their extended and contentious retirement. The average mid-size digital publisher spent a decade watching revenue per thousand impressions fall while technology costs rose and their editorial teams shrank.

Into this environment, several well-funded and genuinely competent ad tech companies arrived with publisher analytics, yield management, and ad operations software. And they charged subscriptions. Flat monthly fees for access to software that would help publishers make more money from their advertising inventory. The publishers, who were already struggling to cover content costs, CDN bills, data licensing fees, and the growing cost of audience development, were asked to add a fixed software expense on top. Just to use tools that might, in a good quarter, generate incremental revenue.

OpenX built what became the second-largest ad server behind Google. Net revenue reached $172 million by 2018. Then in 2019, OpenX shut down its ad server product and pivoted entirely to its SSP and programmatic exchange. The ad server, which required publishers to pay for access, could not compete with Google Ad Manager, which was effectively free because Google extracted its margin from the demand side. OpenX later filed an antitrust lawsuit against Google alleging that the DoubleClick acquisition was used to tie premium publisher inventory to Google’s own stack, driving competitors from the market. The legal argument is legitimate. The underlying economic reality is also relevant: a paid product competing against a free product has a very specific set of problems that good engineering cannot solve.

Yieldex built sophisticated yield analytics for premium publishers. Its customers included The New York Times, CBS Interactive, Pandora, Univision, and The Weather Channel. The CEO Andy Nibley reported gross margins of 65 to 70 percent and 40 percent annual revenue growth over several years. The product worked. In 2015, AppNexus acquired Yieldex for approximately $100 million in cash and stock. Profitable exit. Good outcome for investors. Also a ceiling: eight years of building a category-defining analytics product, serving the world’s largest publishers, and the outcome is an acqui-hire at roughly one times revenue. The subscription ceiling, even for a product with prestigious customers and strong margins, was real.

The companies that scaled in publisher ad tech were the SSPs that took a percentage of programmatic revenue, and the header bidding wrappers that shared in the yield improvement they generated. Magnite, which reported take-rate fees as 88 percent of all revenue in 2024, did not build a $620 million business by charging publishers a monthly platform fee. It built that business by making money only when publishers made money.

There is a sentence that everyone in publisher sales has heard from the other side of the table, delivered by a head of ad operations who is looking at a spreadsheet and then looking at the person across from them: “Our Q3 was soft, so we are reviewing all fixed technology costs.” Every vendor with a flat monthly fee dreads this sentence. The SSP or the yield partner who takes a revenue share never hears it. When the publisher’s revenue goes down, the fee goes down proportionally. The pain is shared. The relationship survives.

* * *

VIII. Klarna Fired 700 People, Rehired Them, and Accidentally Proved the Whole Argument

The Klarna story is usually told as a story about AI replacing workers and then failing to replace them well enough. It is also, if you follow the money, a story about subscription thinking applied to the wrong problem, and what happens when cost and value stop moving in the same direction.

In 2023, Klarna eliminated approximately 700 customer service positions after its AI chatbot, built in partnership with OpenAI, demonstrated it could handle a large volume of customer interactions. The CEO Sebastian Siemiatkowski announced that the AI was doing work equivalent to 700 full-time agents. Projected annual savings: approximately $40 million. The headline was extraordinary. A subscription-SaaS company had traded a labor cost, which scaled with headcount and hours worked, for an AI capability, which looked like it might scale with volume at near-zero marginal cost. This is the dream. You pay once for the capability, the capability runs indefinitely, and the economics improve as volume grows.

The problem was that Klarna was still thinking about the AI like a seat license. You buy the capability. You deploy it universally. You measure cost reduction across the board. But AI capability is not uniform across all tasks. For high-volume, routine queries, the AI was genuinely better than human agents: faster, more consistent, and available at 3am without overtime. For complex, emotionally charged, or judgment-intensive interactions, the AI produced generic responses that annoyed customers and failed to resolve their actual problems.

Subscription pricing logic says: we bought the capability, deploy it everywhere, recover the cost. Usage-based pricing logic says: charge for what works, and let what does not work reveal itself quickly through a bill that falls rather than a survey that nobody reads. The companies that built AI customer service on a usage and outcome model, charging per resolved ticket, knew within weeks which interaction types the AI handled well and which it did not, because the billing told them. Klarna, treating AI as a fixed cost rather than a variable service, had to wait for customer satisfaction scores to deteriorate, for leadership to acknowledge the deterioration publicly, and for an IPO roadshow to change the narrative before correcting course.

By mid-2025, Klarna was rehiring human agents. Siemiatkowski acknowledged: “We focused too much on efficiency and cost. The result was lower quality, and that’s not sustainable.” The company had discovered what the usage-based model reveals automatically: not all output is equal, not all usage generates value, and the only pricing model that honestly reflects this is one where you pay for the value that was actually delivered. Which brings us back to Zendesk, which figured this out before Klarna did.

Zendesk in September 2024 announced outcome-based pricing for its AI agents: $1.50 per automated resolution, declining to $1.00 at high volumes. You pay when the AI successfully closes a ticket without human intervention. When it fails, you do not pay, and you also have a clean signal that it failed: the bill does not arrive. The transparency is built into the pricing model. Zendesk’s incentives and the customer’s incentives point in exactly the same direction. This is what the restaurant analogy was trying to say from the beginning: the best business model is the one where the vendor gets rich only when the customer gets value.

* * *

IX. Salesforce Discovers That a Product Good Enough to Automate Work Destroys Its Own Revenue Model

Salesforce built a $38 billion annual revenue business on the per-seat model. Marc Benioff once used Siebel Systems as the cautionary tale of an incumbent that could not adapt quickly enough when the cloud arrived. He has spent the last two years discovering that historical knowledge of disruption does not make you immune to it.

Andreessen Horowitz published an essay in late 2024 calling out the contradiction directly. They used Zendesk as their example but the logic applies everywhere: when AI resolves a meaningful percentage of customer support tickets, the company needs fewer human agents. Fewer human agents means fewer software seats. The vendor’s revenue falls precisely because the product is working. A product good enough to automate work has destroyed the pricing mechanism that funded the product’s development. This is the subscription model eating itself.

Salesforce’s response was Agentforce, launched at Dreamforce 2024. Initial pricing was $2 per AI conversation. The logic was correct: pay when the AI does work. The execution created immediate confusion. What constituted a conversation? If the AI handled part of an issue and a human finished it, which bucket? A support team running 70 AI-assisted conversations per agent per day could face $20,000 or more monthly in Agentforce fees on top of existing license costs. Of the first 5,000 Agentforce deals Salesforce closed in the first two quarters, only 3,000 paid. The product was right. The pricing was producing buyer paralysis.

By May 2025, Salesforce launched Flex Credits: $0.10 per action, in packs of 100,000 credits for $500. Late 2025 brought per-user licenses at $125 to $650 per month for enterprise editions, because CFOs need a line item that fits in a budget column. By early 2026, Salesforce was running three pricing models simultaneously on the same product, not from confusion but from the recognition that the market has not yet agreed on how to buy AI capability. The usage models drive adoption and growth. The subscription option gives procurement departments something they can approve without a committee. Agentforce reached $540 million in annualized revenue by Q3 FY2026, growing 330 percent year over year. The experiment works. The company is finding its way toward the same place Index Exchange and Magnite started from: revenue proportional to value delivered.

* * *

X. Two Types of Software Company: One Is Fine, One Needs to Go Private Before Anyone Notices

Gokul Rajaram, who built products at Google AdSense, Facebook Ads, Square, and DoorDash, and who has invested in over 700 companies, offered the clearest framework for which software businesses are in genuine danger and which are not. His argument is that the market almost always prices this wrong.

“The software companies that should be the most worried right now is where they are pricing the product based on utility. You need to change your pricing model to be based on outcome, and you need to actually build the product to be based on outcome. It’s easier said than done because literally you’re going from $20 or $30 per seat to maybe charging a buck, or $0.50 or $0.20 per ticket resolved and you don’t know how that’s going to turn out. That’s why I think many of them probably need to go private because they have to make this business model transformation in private. I think it’s going to be hard for them to stay public.” — Gokul Rajaram, Invest Like the Best, 2026

The companies with genuine systems of record, platforms where critical data accumulates over time and where the data itself creates switching cost, are more defensible than the current market narrative suggests. Epic in healthcare. Procore in construction. Toast in restaurants, where payments flow through the platform and create regulatory and operational switching costs that go far beyond software migration. The stickiness is in the data and the financial flows, not in the subscription contract.

The companies in real trouble are the utility layers: tools that perform a task but do not own the data, do not sit in the path of money movement, and do not generate network effects as participation grows. These companies have relied on switching friction as their moat. Switching friction is real. It is also overcome by a sufficiently motivated procurement team with a sufficiently compelling alternative. As AI lowers the cost of building alternatives and raises the quality floor of competing products, the friction required to justify a subscription premium becomes harder to generate.

Rajaram’s prediction that many of these companies will need to go private to complete the pricing transformation is the most honest sentence written about enterprise software in 2026. Changing from subscription to usage-based on a public market stage means several quarters of apparent revenue decline before the model recovers. ARR falls. The new metric is not yet trusted. Analysts downgrade. The CEO is replaced. The strategy is abandoned. The only way to do the transformation correctly is with a longer time horizon than public markets grant. This is not speculation. It is what happened to every major business model transition in technology history.

* * *

XI. The Cost of the Software Fell Off a Cliff. The Price Did Not Follow.

Grady Booch, who co-created UML and has been Chief Scientist for Software Engineering at IBM Research for decades, has seen every cycle that gets described as the end of software engineering. Assembly to high-level languages. Waterfall to object-oriented design. Monoliths to distributed systems. Client-server to cloud. Each transition produced headlines about the death of the previous paradigm, each was actually a rise in abstraction that made the previous layer less visible rather than less real.

“Some of the friction, some of the constraints, some of the costs of development are actually disappearing for you, which means now I put my attention upon my imagination to build things that simply were not possible before.” — Grady Booch, The Pragmatic Engineer, 2026

The cost of building software is falling faster than most people are prepared to acknowledge. The cost to develop a top AI model fell from an estimated $100 million to $5 million with DeepSeek in 2024 and to $30 of compute with Berkeley’s TinyZero in 2025. Software application development has followed a parallel curve. A B2B SaaS product that required fifteen engineers and eighteen months three years ago can be built by five excellent engineers in three to four months today, using AI coding tools throughout.

Five excellent engineers, to be precise. The caveat matters in both directions. AI-generated code without architectural judgment produces the wrong output faster. The engineers who understand what they are building are dramatically more productive. The ones who do not are building more technical debt per hour than any previous generation. The floor has risen. The ceiling has risen too. And the cost that the subscription was originally designed to recover, the engineering hours baked into the product’s price, has fallen so fast that the subscription now contains an increasing share of pure rent rather than cost recovery. The customers can feel it, even if they cannot articulate it precisely. The procurement teams are starting to be able to articulate it very precisely indeed.

* * *

XII. The Subscription Bundle Is Being Taken Apart. Piece by Piece.

The subscription does not disappear tomorrow. Enterprise contracts are multi-year. CFOs built their mental models on ARR and will not abandon the framework in one budget cycle. Sales compensation plans are built around seat count and do not adapt gracefully to usage-based expansion revenue. These are real institutional frictions and they slow transitions that are otherwise economically inevitable.

But the direction is unambiguous. Usage-based pricing among SaaS companies rose from 30 percent of companies in 2019 to 85 percent by 2024. Pure subscription models declined from 65 percent to 43 percent in the same period. Credit-based models, which split the difference between predictable access and variable consumption, jumped 126 percent in a single year, from 35 companies to 79 in the PricingSaaS 500 Index. Seat-based pricing as a share of companies dropped from 21 percent to 15 percent in twelve months alone, while hybrid models surged from 27 percent to 41 percent, according to Growth Unhinged’s 2025 State of B2B Monetization report.

What is happening is that the subscription bundle is being taken apart. For twenty years, the flat monthly fee bundled together access, usage, data, support, and outcomes into one number. Each of those components is now being priced separately and more accurately. Access trends toward free or near-free to eliminate friction and drive adoption. Usage is metered at the action, token, or resolution level. Outcomes are priced at the point of delivery. Support is increasingly automated. The flat fee made economic sense when metering the components was more expensive than estimating them. It no longer is.

The adtech industry has operated on these principles for two decades. Magnite does not charge a platform subscription. Index Exchange does not charge a platform subscription. The software is the relationship. The transaction is the revenue. Publishers who generate no revenue through the platform cost almost nothing to serve in a multi-tenant cloud environment. Publishers who generate significant revenue produce the margin that funds everything. The model self-selects for the customers who matter and scales with their success without anyone calling anyone to negotiate a renewal.

Satya Nadella said SaaS as we know it is dead. He was talking about architecture: business logic moving from discrete applications to AI agents that orchestrate above them. He was also describing, perhaps without intending to, the pricing model that the architecture requires. When software runs continuously as an agent rather than occasionally as a tool, the seat is not the unit of measurement. The action is. The outcome is. The token is. The usage is.

The software is not dying. The service is not dying. The idea that a customer who barely uses the software should pay the same as the customer whose entire business runs on it is dying. And frankly, it was always a strange idea. It just took twenty years of cheap credit, eager VCs, and overworked procurement teams to figure that out.

Somewhere, Brittany is about to get very busy.

* * *